Market was slightly up today due to better economic news. The CDS on Greece went down today to 364 bps, proving my argument that the spread between the CDS on Greece and VIX has to come down. See my earlier post. I argued that either the VIX has to go up or the CDS on Greece has to come down.

As I mentioned before the VIX futures term structure is very steep, and it actually steepened today. The short term volatilties collapsed since February 8. The March VIX futures closed at 20.35, while the April futures closed at 23.45. The difference of 3.1 points is significantly higher than historical medians. Around 90% of the time the spread is smaller than 3.1 points.

So I argue that the spread between the two has to come down. Either the Mar VIX has to go up or the April VIX has to come down.

How could you take advantage of the difference? You could go long Mar VIX and short Apr VIX or sell some ITM Mar VIX puts and some ITM Apr VIX calls.

Any other ideas?

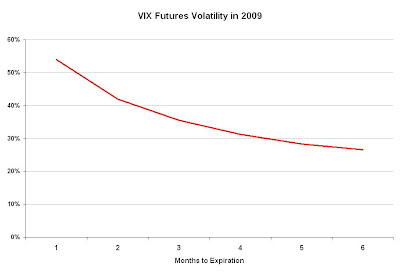

This means that as they get closer to expiration the VIX options implied volatility is increasing.

This means that as they get closer to expiration the VIX options implied volatility is increasing.

Are there any uses for the VXX?

Are there any uses for the VXX? I'm using the high yield OAS as the only input for the model. The R-squared is an impressive 94%.

I'm using the high yield OAS as the only input for the model. The R-squared is an impressive 94%. The fair value for the Dec VIX is about 24.95%. The actual as of 2/19/10 was 23.95%, so about 1% lower than the model tells us.

The fair value for the Dec VIX is about 24.95%. The actual as of 2/19/10 was 23.95%, so about 1% lower than the model tells us.

{kind=link}