This has a significant implication on Greeks. For example, the true theta of an OTM put option is lower than estimated by the Black Scholes model. The reason is that over time the implied volatility of the out of the money put option is going up - the smile is getting bigger.

For example the SPY 2012 Dec 60 Put has an IV of 33.7%, while the 2011 Dec 60 Put has an IV of 35.4%. So over 1 year the IV goes up by 1.7%. The Black-Scholes model says that the theta is 0.0038. If we adjust for the increase in IV over time the theta drops to 0.0028 - a 30% reduction in theta.

On the other hand the IV of an ATM option is going down over time (at least based on the current IV surface), so the theta is underestimated.

To make things even more complicated, the IV surface is not static, it is changing all the time.

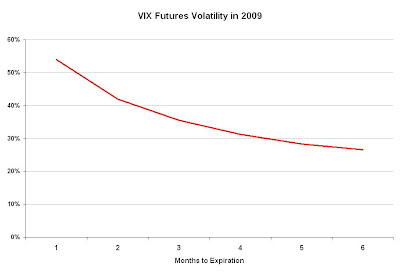

This means that as they get closer to expiration the VIX options implied volatility is increasing.

This means that as they get closer to expiration the VIX options implied volatility is increasing.

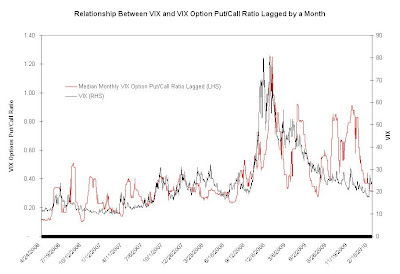

Are there any uses for the VXX?

Are there any uses for the VXX? I'm using the high yield OAS as the only input for the model. The R-squared is an impressive 94%.

I'm using the high yield OAS as the only input for the model. The R-squared is an impressive 94%. The fair value for the Dec VIX is about 24.95%. The actual as of 2/19/10 was 23.95%, so about 1% lower than the model tells us.

The fair value for the Dec VIX is about 24.95%. The actual as of 2/19/10 was 23.95%, so about 1% lower than the model tells us.

{kind=link}